ALEXANDRIA, Va. — There was a lot of good news in the 2023 State of the Satellite Industry Report (SSIR), produced by the Space Industry Association (SIA) and BryceTech. The satellite industry hit $281 billion globally. Satellite broadband revenue grew by 18% and 2022 saw a record 161 commercially procured launches. The report even added a new industry segment to account for the emerging market of space sustainability activities, such as satellite life extension, on-orbit services, debris removal and space situational awareness.

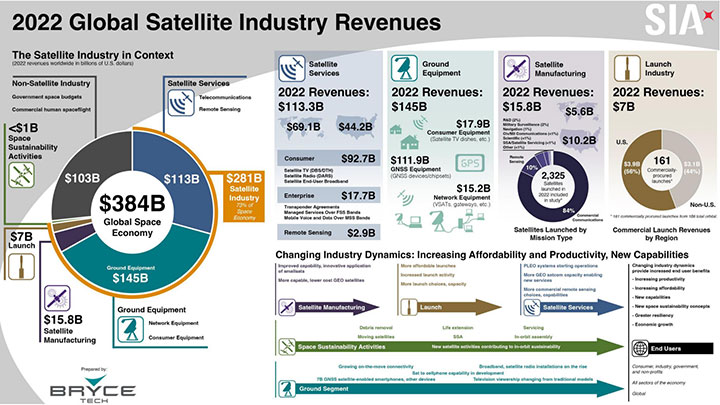

The Space Industry Association released its 26th annual report, produced by BryceTech, on the satellite industry’s economic performance in June 2023. (Source: SIA)

The Space Industry Association released its 26th annual report, produced by BryceTech, on the satellite industry’s economic performance in June 2023. (Source: SIA)

While the report found positive growth in demand across industry segments, one of the more interesting stories is coming from the supply side.

According to the SSIR, the satellite industry could see a near-tripling of total GEO capacity by 2026. Today, there are around 3.5 Tbps of cumulative high-throughput satellite (HTS) capacity on orbit, following a significant deployment in 2021. In the coming years, operators plan to deploy an additional 6 Tbps of capacity, based on GEO satellites under contract and in development. Within that same time, mega-constellations are scheduled to enter service or expand, and LEO capacity could potentially exceed 180 Tbps.

In addition to a massive addition of capacity, the SSIR also highlighted the ongoing affordability trend, with lower costs affecting all parts of the industry. Launch costs were down 36% over the last decade—and revenue was up 23% for the year. Since 2013, there has been a 90% reduction in manufacturing costs per Gbps of throughput thanks to advanced manufacturing processes, software-defined payloads and spot beam technologies. Cloud integration and “as-a-service” offerings have made the ground segment less expensive.

Amid growing capacity and lower costs, the SSIR also documented a decline in satellite service revenues.

“This is part of a trend toward increasing affordability,” Fletcher Franklin, Senior Program Manager at BryceTech told Constellations. “The more advanced GEO satellites with higher capacity are being deployed and the cost of those satellites has been dropping. So, those satellites are delivering more capacity per dollar, which reflects the increasing value that the satellite industry is delivering.”

Much of the losses in satellite service revenue were driven by satellite TV, as consumer preferences shift to content streaming and low-latency, bandwidth-intensive applications. These losses also impacted enterprise revenue associated with transponder leases for raw capacity.

There was significant growth in satellite broadband and satellite radio, as well as value-added managed enterprise services, like in-flight, maritime mobile, broadband and IoT. However, at this time, the growth of those services was not enough to offset the multibillion-dollar losses.

Finding the Right Alignment

The changing landscape of satellite services and the dramatic growth in GEO and LEO capacity raises important issues for the industry, including how and where to stimulate demand to absorb so much new capacity. This can be seen in the growth of new markets for managed services as well as expanding service agreements among different industries, like telecommunications, energy, transportation and logistics, agriculture, IT and government.

Still, questions remain about the size of demand, the risks and benefits of commoditization and how much time it will take for service revenue to catch up with CAPEX. Because, even as satellites become more affordable to produce, long-term constellation operations are still CAPEX heavy.

“The ability to deliver more capacity to customers based on a lower cost is better value. But profitability has a lot of components,” Franklin noted. For example, a GEO operator may have a higher upfront cost, but that trades against 15 years or longer of revenue-generating service life.

The satellite industry continues to become more affordable, particularly as a measure of increased throughput per kg of upmass. This image shows the Intelsat 33e high-throughput communications satellite. (Source: Intelsat)

The satellite industry continues to become more affordable, particularly as a measure of increased throughput per kg of upmass. This image shows the Intelsat 33e high-throughput communications satellite. (Source: Intelsat)

In many cases, lower production costs and greater HTS capacity has been passed on directly to end users of certain services. According to NSR research presented in March, a doubling of total HTS capacity in 2017 led to a 50% drop in prices for GEO broadband consumers the following year.

NSR analysts noted the lower prices also make it more feasible for satellite to “move down the value chain and compete on a retail level” in areas that were unthinkable a decade ago. They also cautioned against undercutting prices too far in response to oversupply, leading to “thinner margins” and eroding profitability.

Amid concerns about oversupply, there are cases where operators are seeing capacity grabbed up faster than they can deploy it. Space Intel Report recently reported on the insatiable demand for satellite broadband capacity in Indonesia in connection with the Bakti universal service obligation program. By the end of the year, PT Pasifik Satelit Nusantara (PSN) will have deployed two HTS with a combined capacity of 330 Gbps. Yet, officials are realizing that will not be enough to meet connectivity goals and may have to scale back deployment plans.

It will take time to align demand with capacity and to build a market for new and expanded services. The overall global space economy grew by 2% last year and it is still in its youth. Technologies that have been under development for decades are finally emerging as deployed capabilities, with a potential that is hard to deny.

Explore More:

Podcast: Big Demand, Smallsat Manufacturing and New Satellite Services

BCG Space Executive Explains Growth Trends for Value-Added Space Services

Podcast: Mainstreaming Satcom, Convergence with Telco and Connectivity Everywhere

Affordability Is Transforming the Satellite Industry: How Each Segment Is Keeping Up