PARIS — The UK-based Seraphim Space Investment Trust went public on the London Stock Exchange in July with 15 startup space companies in its portfolio. It added six in the ensuing months and another earlier this year.

Managing Director Mark Boggett says the goal is 30-50 companies to provide sufficient diversity to allow Seraphim to ride out market downturns and offset investments that go sour with the winners.

Under the law governing this kind of trust, Seraphim duly laid out to investors the level of risk implicit in the trust’s goals, going to far as to spell out how much money they stood to earn — or lose — depending on different performance scenarios — Favorable, Moderate, Unfavorable and Stress.

The company’s Key Information Document, required by law, includes a handy “risk indicator” advising that, on a risk scale of one to seven, the Space Investment Trust risk level was five, assuming investors retained their stakes for five years.

Boggett says that for its part, the fund is investing for the long haul — buy-and-hold to the extreme, given the long road to profitability, for many of these companies.

Does this seem old-fashioned to you? If so, you may have had a ball during the recent SPAC transactions in the U.S. market for space startups.

Boggett has nothing against SPACs, but does reproach some companies’ managements for inflating forecasts. They are now paying the price as they miss their targets. He discussed his fund’s approach.

Mark Boggett. Credit: Seraphim video

Mark Boggett. Credit: Seraphim video

Does the SPAC process gave companies too much margin to make pie-in-the-sky revenue forecasts?

I can’t imagine that too many investors who are not sophisticated are investing into SPACrelated companies. I don’t think it’s something that is owned at the retail-public level.

It’s for at companies that aren’t quite right for an IPO, an alternative to a traditional IPO. The fact that it has different requirements doesn’t worry me.

What has gone wrong, and there are companies that have now been held accountable for this, is that there has not been enough diligence on the numbers that have been presented. The sponsors didn’t do even the most basic of the diligence you would expect them to do.

I think that’s part of the efforts of the SEC [the U.S. Securities and Exchange Commission] and who things are now taking 4-6 months to go through, because there is more of a focus on that.

SPACs have been around for many years. They became highly fashionable during a very short window of time. A number of them were unscrupulous and didn’t do their jobs properly.

What about the high redemption rates we’ve seen in many SPAC companies once they are public?

The important investors are the PIPE investors. These are the ones investing for the long term. Those that invested into the SPACs are the hedge funds, short-term investors by their nature. What is really important is the PIPE investors. These have pretty much packed up and gone away when it comes to SPACs at the moment.

We need to see them return with their appetite to invest in these types of companies before you’re going to start seeing a decent flow of SPACs again.

So for me it’s not about the redemptions, it’s about the health and vibrancy of the PIPE market — particularly in the environment we are in right now, with a sell-off of technology as we entered the new year.

Many of the SPAC companies published outrageously optimistic, hockey-stick growth forecasts. And they are not making these numbers.

It doesn’t give much confidence in their longer-term projections if they can’t meet their shortterm projections, does it? That’s why some of them have been so badly marked down. They didn’t meet the first numbers they presented.

Spire is one of those, and you doubled down on your investment, taking advantage of the share-price drop.

The reality is that this company is growing quickly. It’s got more than 100 satellites in orbit, it’s uniquely positioned. It’s doing very well.

Leaving Spire out of this because it’s one of your portfolio companies, what’s the reasoning behind pumping up growth forecasts when the reality is already good?

You have to put that at management’s feet. The advisors are responsible for keeping in check the long-term hockey stick, making sure it’s at least in the realm of believability. But it’s down to the management team to make sure they can hit the first years’ targets, because they are not going to have a successful life on a listed market if they cannot predict the numbers.

For entrepreneurs and companies that might consider listing, the SPAC experience has put most of them off wanting to do it. Those that haven’t gone through the SPAC process don’t want even to consider doing it now.

That would move them toward a standard IPO?

A standard IPO, or just staying private for a longer period. The SPAC opportunity was there, and those quick enough to grab it did grab it. And it worked. They got exactly what they needed in financing to build out their constellations. Even if the share prices are down, the management team have got to be delighted that they have the capital they need to drive the business forward. The fundamentals will come through as they grow the business.

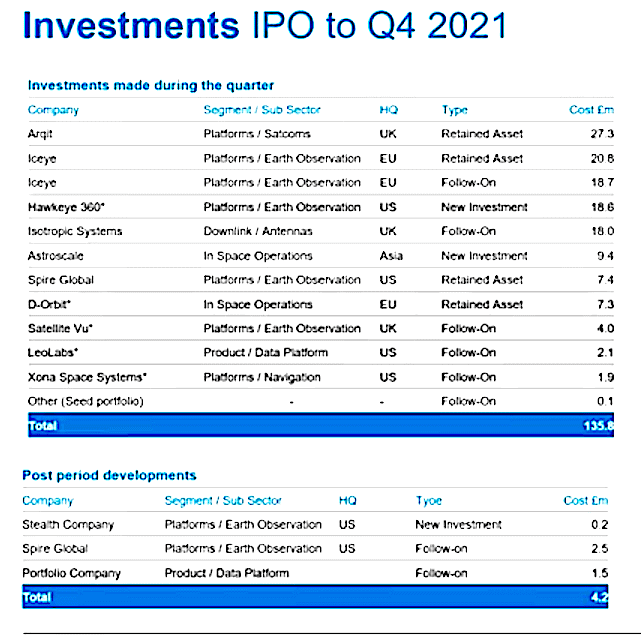

These are investments that Seraphim Space Investment Trust made between its July 2021 IPO and the end of the year. Credit: Seraphim

These are investments that Seraphim Space Investment Trust made between its July 2021 IPO and the end of the year. Credit: Seraphim

If you believe that the only people who got run over by the missed revenue forecasts and the stock collapse were hedge funds and not retail investors…

I am very close to what goes on in this market, having been invested in so many of them. Those that are playing the secondary market in these companies, after the stock has combined, are the hedge funds. They are driving the share prices up and down, on thin markets. They can make significant gains in both directions, until they get bored with it and move on to the next.

A regulatory hand somewhere in there would not have been a good thing?

The SEC has actually now come in and put a massive hand break on the market and are only allowing SPACs to trickle through after they have had a huge amount of scrutiny. The SEC has done everything you would expect them to do.

For some of these companies, it would take a deep level of technical knowledge to discern what was real and what wasn’t — whether a test payload functioned entirely as expected on orbit, etc.

This is why I think companies that are going to get through successful SPACs in the future will be those that have more evidence that they have revenue and that their technology is working and customers are buying it. I don’t think customers will be willing to back companies that are all speculation.

That’s a thing of the past.

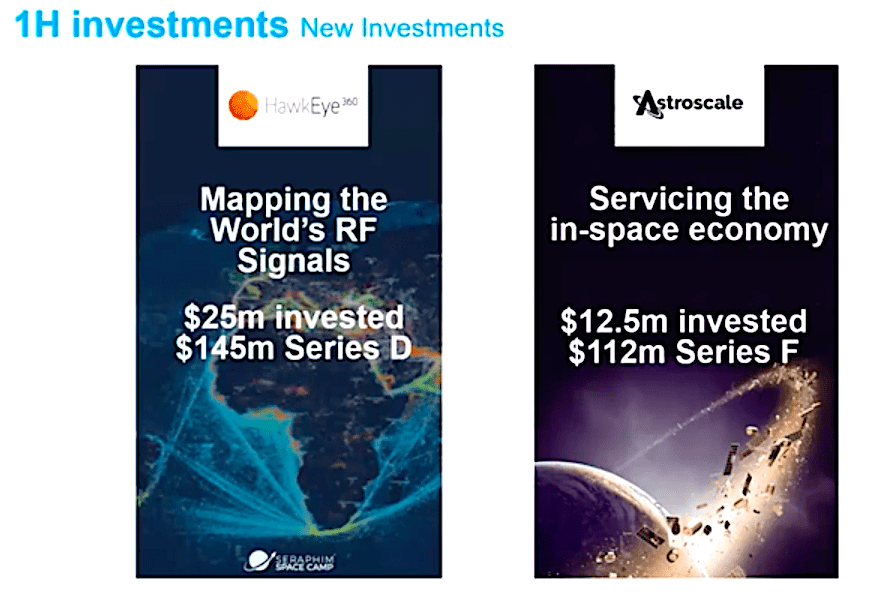

Seraphim usually takes relatively small positions in funding rounds. But there are exceptions, such as these investments in RF surveillance company Hawkeye 360 and satellite-servicing/debris removal startup Astroscale. Credit: Seraphim Space Investment Trust

Seraphim usually takes relatively small positions in funding rounds. But there are exceptions, such as these investments in RF surveillance company Hawkeye 360 and satellite-servicing/debris removal startup Astroscale. Credit: Seraphim Space Investment Trust

Aside from the reduced enthusiasm for SPACs, has your market view changed given that the Fed is going to raise interest rates to bring down inflation? Are we in a different environment now?

Space is a long-term, multi-decade market that is really only just getting going. We are really at the foothills. Even the most advanced space companies still have low revenues. Regardless of the macro environment we’re in, these businesses are going to continue to exhibit strong growth.

The factor that will change is the valuation it will take for investors to continue to provide capital.

‘Investor enthusiasm, despite everything, remains high’

Investor appetite to participate in investment rounds, at each stage of the space ecosystem, remains very positive. We are still closing seed arounds, A, B, C, and D rounds. Investors are not dropping out.

The release valve is the valuation. Investors will want to adjust that for the macro environment. That usually takes a little longer to work through in the private market than it does in the public markets.

The good news is that the public markets are very clear. There is a massive sell-off in technology and it’s unlikely to come back in the near term given everything else on the macro horizon.

Investors like us will be using that as a reference point when they are talking about term sheets on the investments they make.

We’ll see valuations moderate as a consequence but deals will continue to get done. There is just a growing belief that this is a long-term growth market. In particular, investors are getting their teeth into the fact that there is a big climate angle to space.

I think one of the reasons our share price hasn’t significantly fallen since the Ukraine news is that people recognize the dual-use aspect of space and how defense and intelligence are looking at using these commercial companies to help them develop their capabilities.

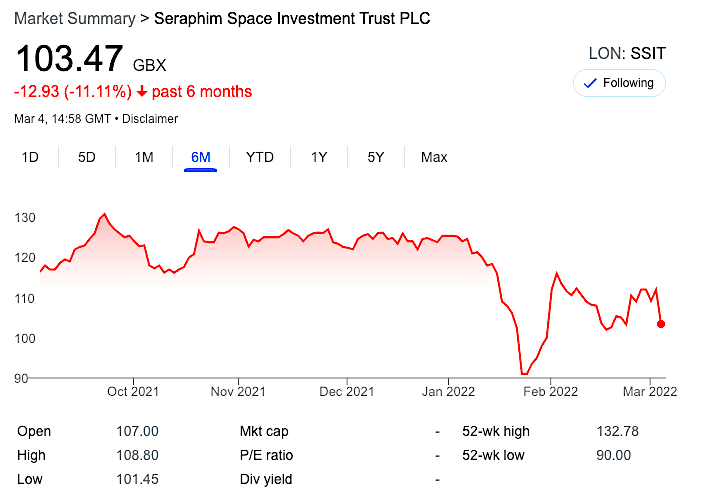

Credit: Google Finance

Credit: Google Finance

What happened to your stock in mid-January to cause it to dip suddenly?

A: Two things happened at the same time. The sell-off on the technology stocks happened over several days and coincided with the end of the lock-in period for investors in my old venture fund, who were provided with shares in our investment trust as payment for their holdings in the previous fund.

We seeded our IPO with 15 companies that were acquired from our old venture fund. All of that was paid for in stock.

So you had general sellers and specific sellers. After that happened, the stock went down to about 90 pence and the brokers arranged for me to speak with many of our shareholders and the price then regulated back up.

Seraphim runs space camps for startups to prepare them for the task of fundraising and managing growth. Credit: Seraphim

Seraphim runs space camps for startups to prepare them for the task of fundraising and managing growth. Credit: Seraphim

Your shareholders are mainly institutional?

About 20 shareholders account for 80% of the stock.

You see this as a multi-decade growth story. Investors often don’t want to wait that long. Do you have an average number of years that you hold a stock?

We are saying from the get-go that these are long-term growth investments that are going to take 10 years to start maturing. It will take years to get the digital infrastructure up, get customers used to using it and then adopting it and embracing it in full.

That is probably a seven-year journey. We’re seeing that with the market leaders already. Look at Planet. It’s taken them years to get to where they are today and yet I still think they are five years away from really being able to show profitability.

The fact is that this digital transformation is under way and that space is part of it. Companies that focus on the space options available to them, and get ahead of their competition by lowering their costs in embracing, will get us through this 2-3 years to return to the appetite for growth.

Is your portfolio diversified enough to be able to absorb the investments that go bad by more than compensating with the winners?

We have 22 companies in the portfolio at the moment. We have said we are going to go to between 30 and 50. You need over 20 to have a portfolio that is considered to be diversified. We are diversifying by country, by stage, by category of space…

Even between two countries in the euro zone?

You have a difference in the level of bureaucracy. How easy is it to hire and fire? This has a direct impact on how investments can work. And to what extent can they attract international talent? It does make a difference between countries.

The part of space we are focused on is centered on digitalization and how that is going to affect the planet. That’s really where we spend the majority of our time and focus.

Any areas you avoid?

A new type of space investment that we have not really been looking at includes space hotels, space travel, lunar activity, in-space manufacturing. From a commercialization perspective they are further away.

They were much further away in 2016, when we first started doing this. Those companies are now moving to the edges of our interest so we can start thinking of them. At some point, in five years’ time, that could be the core area of focus for us.

Credit: European Commission

Credit: European Commission

You are in the UK. Can you still be part of the European Commission’s Cassini Fund, a billion-euro VC fund for space that should be operational later this year?

I don’t see why we couldn’t. I am sure we will find a way to work alongside them. What they require is that for every euro they put in, they need to see two euros invested in Europe. Provided that you can demonstrate you are able to do that, then they can invest in funds that are outside the European Union.

Whether they will is a different matter. But they can. Despite Brexit, we consider ourselves European and we should be able to find a way to make this work. Regardless of whether we get involved, we are listed, and accessing money is not something I lose sleep over.

What will be great is that this [Cassini Fund] will be a significant amount of money coming into a market that I am passionate about and believe in. One way or another this is going to have a big impact and we will be playing a role.

Assuming they don’t invest in multiple smallsat launch startups, a crowded area you have avoided.

The EIF [European Investment Fund] knows a thing or two about deploying money and giving it to the best managers. What you are going to see in most cases is well-regarded, generalist investors that have agreed to invest a certain percentage of their fund into the space domain. That’s how I think you’ll see most of the money going out. I don’t think it’s going to be through dedicated space funds that need to chase everything.

Read more from Space Intel Report.