Originally published by Northern Sky Research on September 12, 2023. Read the original article here.

The launch bottleneck is not a new phenomenon for the satellite industry. However, the available and operational vehicles are few and very busy or experiencing failures, thus creating the shortage we know today, which is limiting access to space. Even giants struggle to launch. Indeed, in early August, Amazon had to change launch vehicle yet again, to avoid delayed deployment of its Project Kuiper prototype satellites. It had signed launch contracts with multiple LSPs to avoid such an incident, but despite this foresight, the next-generation of launch vehicles of all of its contractors are delayed. However, if a giant like Amazon faces such difficulties, then what does this shortage mean for the rest of the industry, and who will be impacted the most?

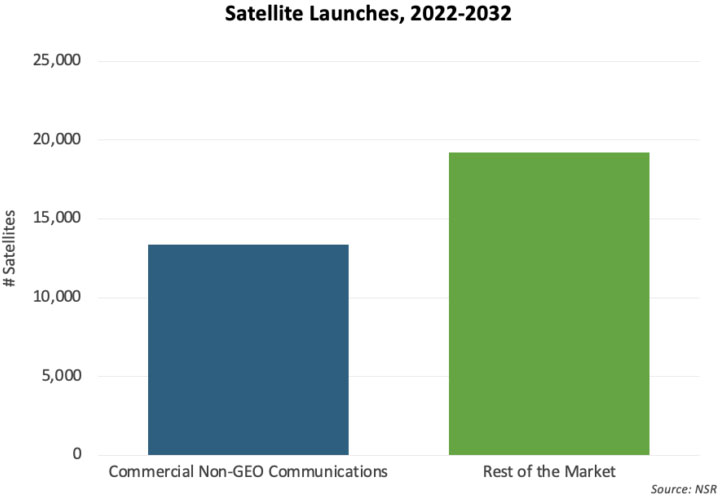

NSR’s Satellite Manufacturing & Launch Markets, 13th Edition report forecasts over 32,000 satellites to be launched over the next decade, generating $134 billion cumulative revenues in launch services. Out of all the satellites expected to be launched, no vertical represents a higher risk than Commercial Non-GEO Communications.

Non-GEO Dictates the Direction

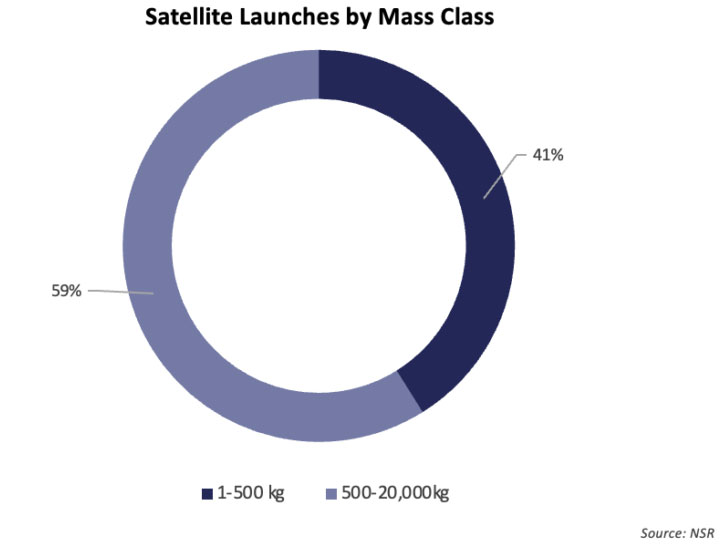

Commercial Non-GEO Communications is a high-profile vertical, featuring most constellations expected to launch by 2032, representing 41% of the total number of satellites to get to orbit over the next decade.

Moreover, revenue-wise, this vertical is forecast to generate $16 billion in launch revenues, while Commercial Non-GEO EO, which also features many satellite constellations, is expected to generate only $5.2 billion, nearly 3-times less. Higher-mass satellites, more satellites per constellation, and premiums to be paid for priority launch lead Communications to triple the launch revenue opportunity compared with Earth Observation.

Where is the Blockage?

Taking a closer look at the Commercial Non-GEO communications vertical, satellite operators aiming to test their prototypes and medium/emerging satellite operators will struggle the most.

The mass class under 100kg features the highest number of prototypes. These prototypes require little space within a rocket and have little resources, making them secondary customers on launches. As an outcome, they might be delayed or might not be able to secure launch and be left on the shelf until access to launch improves.

Secondly, the 100-500kg mass class, which has most satellite constellations, drives the highest demand of the vertical and generates the highest revenues. There is a strategic importance for these missions, for which satellite operators might need to pay a premium price to secure launch, which reduces margins.

Who Can Afford it?

In many cases, Government/Military missions and large GEO satellites have higher budgets and will be favored over other missions as a priority customer. However, medium-size to emerging satellite operators might represent the highest demand but might be a lower priority for launch, as they have less resources and usually need little space for launch, hence are often treated as secondary costumers in a rideshare launch.

At the same time, commercial Non-GEO communications satellite operators are driven by their licenses requirements, which puts their deployment on a time limit, as FCC rules require them to launch 50% of their satellite constellation in a set amount of time, which put approval of the case for Amazon on condition that it launches half of its constellation by mid-2026.

In the best-case scenario, late deployment of satellite fleet might delay and/or reduce downstream revenues. But a more severe outcome would be reduction of constellation fleet, which could downsize coverage and impact downstream revenues, and even perhaps lead to losing licenses to operate. Meanwhile, satellite operators with reduced constellation fleets, would have even less of a priority as a costumer in rideshare missions and would need to find alternatives, of which there are still very few operational today.

The Bottom Line

The launch bottleneck is expected to impact more the constellations operators with satellites in the 100-500kg mass range, in the Commercial Non-GEO communications vertical. Unable to handle limited launch options, higher launch costs and deployment time limits that licenses have added, some satellite operators might be affected negatively by this situation. For these satellite operators to survive in this market, they will need to prepare delaying their constellation deployment and renew their licences in this current launch shortage until accessibility improves.

Originally published by Northern Sky Research on September 12, 2023. Read the original article here.