PARIS – Internet connectivity has become, more than ever before, a lifeline for working, learning, networking and accessing essential services. An estimated 5.3 billion people (roughly 67% of the global population) used the Internet in 2022, a number that has doubled in the past eight years. Universal connectivity may not be a distant prospect in mature markets, where more than 90% of the population uses the Internet, but the situation is different elsewhere.

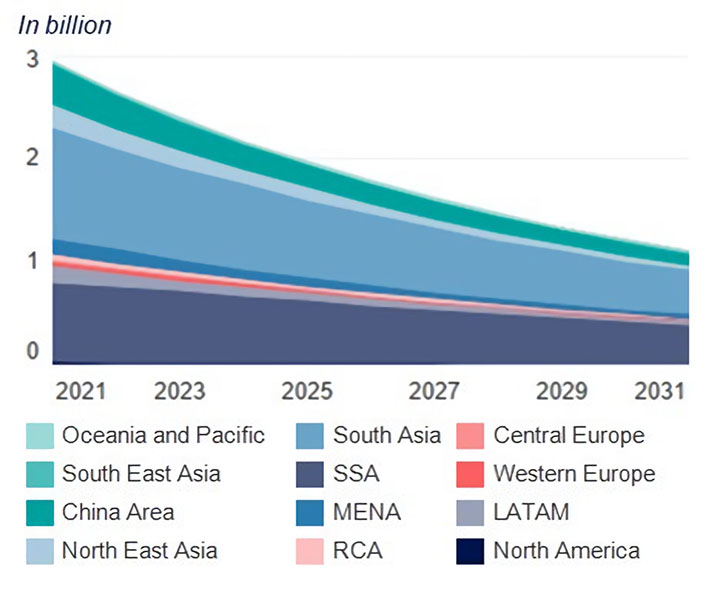

Despite the significant progress observed recently, 2.6 billion people remain unconnected, with Asia Pacific and Sub-Saharan Africa accounting for 85% of that total. This unserved market represents a $74 billion untapped opportunity for service providers, as highlighted in the 2023 edition of Euroconsult’s Universal Broadband Access report. Internet access lags far behind in least developed countries (LDCs) and landlocked developing countries (LLDCs), where just over one-third of the population is connected. India alone accounts for one-quarter of all unconnected people.

Evolution of Unconnected Population by Region (Source: Universal Broadband Access, Euroconsult)

Evolution of Unconnected Population by Region (Source: Universal Broadband Access, Euroconsult)

Satellite Well-Positioned to Bridge Digital Divide

Satellite should play a key role in rural areas to help reduce the digital divide. Satellite is and is expected to remain the best cost-effective option for low-density areas where terrestrial network deployments are not economically feasible. These areas currently account for a significant share of the remaining unconnected population. Wi-Fi hotspot services, in particular, are a low-cost solution that is likely to be viable even in some of the most remote areas.

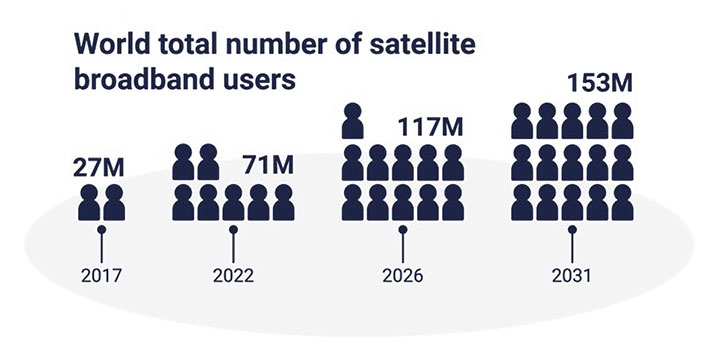

(Source: Universal Broadband Access, Euroconsult)

(Source: Universal Broadband Access, Euroconsult)

In recent years, data usage per user has grown considerably with increased usage over home connections and a larger number of mobile apps and social media interactions. Satellite services have adapted to the trend, with both download speeds and data limits (in GB) regularly improving. A progressive shift towards unlimited data plans has occurred, especially with the arrival of new generations of satellites and increased data requirements for activities such as HD video streaming.

Currently, most service providers that offer unlimited services impose soft caps reducing the speed and quality of the data due to network congestion and fair usage (Starlink being the exception). These caps suggest that the need for satellite data visibly exceeds the currently available supply.

Device and Service Cost Impediments

Despite the availability of better-quality satellite services, several inhibitors for the expansion of satellite use remain. Two of the most important are the price of services and the affordability of internet-connected devices. For satellite to further expand its addressable market, service prices would have to decrease below current levels. The rollout of constellations and next-generation HTS satellites should allow this to become reality. In coming years, available satellite capacity is headed towards a dramatic increase. Growth will be largely influenced by NGSO constellations (e.g. Starlink, OneWeb). The satellites from NGSO constellations are projected to collectively account for more than 90% of the total available satellite capacity in 2028. Several large GEO satellites are also expected to be used to help reduce the digital divide, with key projects including Hughes’ Jupiter-3, PSN’s Satria and Viasat-3.

With the new generation of satellites, the cost base of capacity is expected to fall to less than $5 per Mbps per month post-2025. Improved economics should contribute to the decrease in capacity pricing, a key element for the development of the highly price-sensitive satellite universal broadband access market. They will contribute to the availability of “better quality” packages for end users, such as unlimited plans and higher data rates as well as to the increasing affordability of entry-level satellite services. This should allow satellite to be increasingly competitive with terrestrial services in rural areas.

An example of how improvements in satellite technology have allowed operators to provide lower-priced services is Kacific with its Kacific-1 satellite. The satellite reuses the same spectrum (frequencies) multiple times, which allows Kacific to deliver greater spectral efficiency and therefore lower the cost per Mbps compared to traditional FSS satellites. Today, the price per GB with Kacific exceeds the affordability targets set by the ITU and UNESCO. Kacific’s Community WiFi service, which was created to allow anyone in rural villages of Southeast Asia and the Pacific Islands to access affordable satellite broadband internet, offers pre-paid vouchers for less than US$2 for 1GB.

User equipment cost remains a significant driver of Total Cost of Ownership (TCO) and a key reason why so many people remain unconnected. Therefore, policies such as those adopted by major satellite service providers may be necessary to further expand satellite-connected users. In 2023, Starlink modulated the price of equipment to account for customer purchasing power. Similarly, Viasat implemented its Digital Empowerment Initiative in Latin America, providing laptops to organizations working to bridge the digital divide.

Opportunities to Expand Universal Broadband Access

In coming years, another key factor for the rapid expansion of satellite broadband services will be accelerated government support. This is often a key remedy for broadband market failures in areas where it is difficult to close business cases for extending terrestrial network coverage on a purely commercial basis. Recently, a growing number of public-private collaborations involving satellite operators have been announced. One of the latest was in early 2023 in Argentina, where the government financed the purchase of computer equipment and two VSAT antennas per locality as part of the “Mi Pueblo Conectado” initiative in partnership with ARSAT.

The cost base of satellite capacity is expected to fall to less than $5 per Mbps per month post-2025, contributing to the development of the price-sensitive satellite universal broadband access market. (Source: Shutterstock)

The cost base of satellite capacity is expected to fall to less than $5 per Mbps per month post-2025, contributing to the development of the price-sensitive satellite universal broadband access market. (Source: Shutterstock)

Big Tech companies, which often bring much-needed innovation and agility to a market, could also play a role in extending connectivity. There is an inherent market driver for Big Tech. In launching initiatives to connect the unconnected, they are extending the addressable market for their own internet-based services. Microsoft’s Airband Initiative is particularly active in Africa, integrating international public entities, like USAID and energy firms in their approach, in addition to operators and Internet Service Providers. In December 2022, Viasat became the first satellite partner to work with Microsoft Airband.

Other opportunities exist for satellite to contribute to bridging the digital divide, including the direct-to-device (D2D) market. The D2D satellite service landscape is gaining momentum, supported by new regulations and FCC rule-making, as well as the development of new 5G standards through 3GPP to more seamlessly integrate satellite into terrestrial networks.

While the addressable market for D2D services could span into the billions of subscribers and devices within several years, the ultimate captured market is clouded by uncertainty surrounding a mix of factors including regulatory access, technology development and access to funding.

Global Broadband Initiatives

There is a worldwide agreement that providing access to connectivity to everyone is crucial for achieving sustainable development, economic progress, environmental stability and social inclusion. The Broadband Commission, a joint initiative by the ITU and UNESCO, set a goal of achieving universal broadband access connectivity. This involves all countries having a national broadband plan or strategy in place or including broadband in their definition of Universal Access and Service (UAS). In 2022, 155 countries met this target. If governments around the world increasingly implement broadband plans, this is likely to increase network availability, affordability, safety and broadband adoption in countries.

Despite “Internet for all initiatives” and the availability of lower-priced services in coming years, Euroconsult expects that at least 1 billion people could remain off the grid by the early 2030s, as the last unconnected people will be the hardest to serve. For the “last billion”, initiatives such as the provision of free smartphones and free internet connectivity would be mandatory to one day bridge the digital divide. A good example of such an initiative is the partnership in India in 2022 between the state of Rajasthan and commercial players including Reliance Jio, Bharti Airtel, Samsung and Nokia.

In coming years, strategies and policies to enable further broadband adoption and accelerate digital inclusion will be key to transition to a more connected world where bridging the digital divide becomes a possibility. Within the global push toward universal connectivity, satellite should play a central role, with the deployment of next-generation satellites and constellations expected to be a game-changer.

Read more from Euroconsult.

About the Author

Dimitri Buchs is a Managing Consultant of Euroconsult, based in Montreal, Canada. He specializes in digital TV and broadband markets and their impact on the satellite business. His key interests also revolve around satellite communications markets. Dimitri is the editor of Euroconsult’s premium research report “Satellite Connectivity & Video Market.” He is also the editor of “FSS Operators: Benchmarks & Performance Review” and Euroconsult’s “Universal Broadband Access” report.

Explore More:

Podcast: IEEE on Space-Based Networking and the Broadband Communication Ecosystem

Kacific CEO: Closing the Digital Divide Across the ‘Ring of Fire’

Podcast: Tom Stroup on 5G, Satellites and Connectivity Everywhere

US to Spend $42B on Broadband Equity: Will Satellite Be Included?