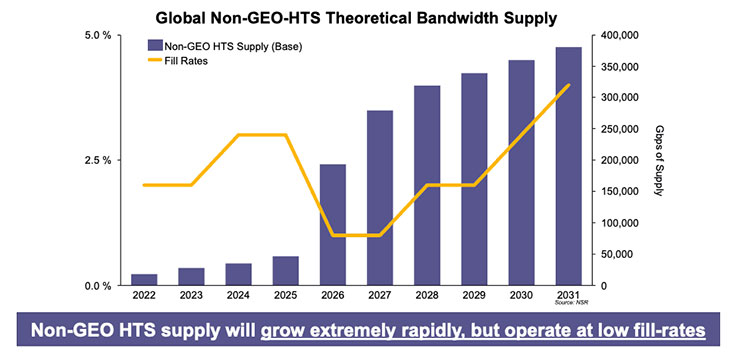

A 5% fill rate? Can even Starlink and Kuiper sustain multibillion-dollar constellations with that? (Source: NSR)

A 5% fill rate? Can even Starlink and Kuiper sustain multibillion-dollar constellations with that? (Source: NSR)

PARIS — For satellite service providers and hardware builders, the question is not complicated or new:

What’s your survival strategy when SpaceX’s Starlink and Amazon’s Kuiper constellations are fully operational?

Both appear intent on creating their own ecosystems with proprietary standards, so forget selling much to them. Both appear able to go for many years, spending billions of dollars, before becoming profitable.

Several possible answers were offered during The HTS Roundtable, organized Dec. 8 by c21-virtual:

- Accept that the connectivity world will divide into several fiefdoms, with small satellite fleet operators banding together to create their own standards as they focus on their home markets using high-throughput and software-defined satellites to lower cost.

- Hope that the 3GPP standards body, perhaps as part of its Release 18, imposes a standard that will allow the satellite sector to reach the scope and scale promised by 5G, and that this standard cracks open Starlink and Kuiper.

- Swallow your pride and surrender to whatever M&A opportunity offers the best protection through volume, at least in markets not targeted by Starlink and Kuiper.

Gilat Satellite Networks wants to reinforce links with its current customers, including fleet operators SES and Intelsat, which may or may not provide safe harbor.

“It is very hard to anticipate what will happen four or five years from now,” said Gil Elizov, Gilat’s vice president for products. “The change is too big to evaluate at this point. I am pretty sure we will see more and more mergers. Some of the players will need to merge to compete with the big players like Amazon and Starlink. There is no other way.”

Gilat, accustomed to be an outsider looking in with respect to the proprietary networks of Viasat Inc. and Hughes Network Systems.

Cristi Damian, vice president of Comtech Satellite Network Technologies, said the lure of a much larger market in a 5G world might be enough to force standardization on those not inside Starlink or Kuiper.

“We have 3GPP study groups working on standardization but at the satellite level there is no such thing,” Damian said. “it’s really needed — unless we are going to end up with a fractured system where one operator cannot communicate with another. That would be a pity.”

The market is still waiting to find out if the low-latency advantage of non-geostationary satellite networks will find a market large enough to justify the additional cost of these constellations and their user equipment.

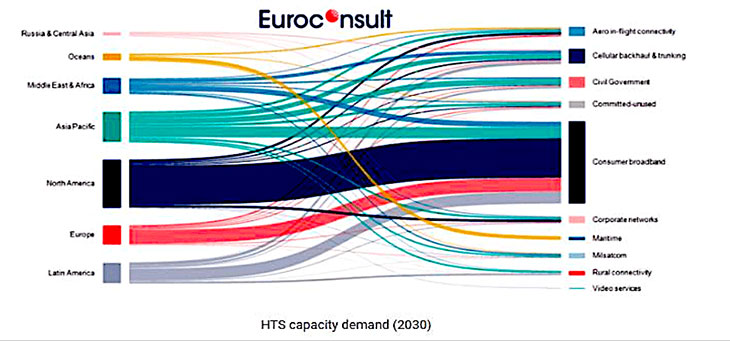

A challenging demand picture to 2030 from Euroconsult…

A challenging demand picture to 2030 from Euroconsult…

Jaime Reed, vice president for space data platforms at CGI Group, said low latency offers a superior user experience, but that much of it is psychological: In fact, a large portion of any company’s bandwidth demand is not latency-sensitive.

“The majority of traffic in an enterprise is not real-time data,” Reed said. “It’s things like data-based replication and back-office data. None of that is latency-critical. And the majority of traffic even on mobile networks is people watching videos, which is not latency-sensitive at all.”

If low latency is not that important, operators of satellites in geostationary orbit that renew their fleets with software-defined and high-throughput satellites will be able to offer ever-lower prices and maintain market share, he said.

What about LEO fleet operators in the competitive mix? Eutelsat has said its purchase of OneWeb is a way of offering the best of GEO with a low-latency, global LEO network.

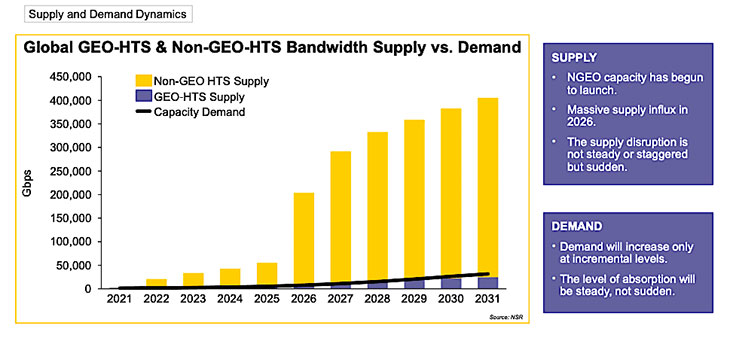

…and a similar conclusion from NSR. (Source: NSR)

…and a similar conclusion from NSR. (Source: NSR)

Canada’s Telesat has said reservations for its future Lightspeed LEO constellation have not fallen away even as Lightspeed is delayed pending closure of its financial backing.

Jiby Jacob Thayyil, Lightspeed’s project director, said coming to service several years after Starlink and OneWeb, and around the same time as Kuiper, is actually an advantage because the first-mover fleets will have prepared the market for what LEO can and cannot do.

He noted that in some regions, Starlink’s early performance has suffered from congestion as more people sign up. “You start seeing a drop in performance,” Thayyil said.

Lightspeed hopes to avoid most head-to-head competition with Starlink and Kuiper by sticking to a B2B model and using a wholesale approach that does not, unlike Starlink and perhaps Kuiper, threaten network operators or service providers “rather than going after their bread and butter.”

At other industry forums, some regional fleet operators have said they will rely on their government regulators to impose restrictions on Starlink, Kuiper and OneWeb as a condition of market access, if not shutting out the global constellations altogether, as China and Russia may do.

EchoStar Corp. Chairman Charlie Ergen told investors in February that the company was still flummoxed about how to confront Starlink and Kuiper, which he said are so large they “create their own set of economics.”

Ten months later, the company is still looking for a strategy.

Read more from Space Intel Report.